A hidden threat to stability

Note

The modern global economy runs on digital rails, where speed, reliability, and security are fundamental necessities. However, beneath the glossy facade of digitalization in the traditional banking sectors of Europe and the United States, there is a ticking time bomb - critically outdated IT systems and poor user experience. This technological debt, accumulated over decades, has today turned into an existential threat that undermines customer trust and opens the door to disruptive innovations, such as the solutions offered by DARCA.

This study presents an in-depth analysis of two interrelated problems:

- Weak mobile and online banking: Outdated interfaces, poor design, and limited functionality that fail to meet the expectations of modern users.

- Outdated IT systems: Monolithic and inflexible core systems that lead to frequent outages, vulnerabilities, and an inability to implement innovation.

The goal of this report is to use concrete figures and statistics to prove the scale and systemic nature of these problems. We will demonstrate how technological failures lead to colossal financial losses, destroy customer loyalty, and create a massive, unmet demand for modern financial tools. We will prove that solving these problems is not a matter of evolution, but a requirement for revolution - one that DARCA is ready to lead.

Table of contents

- Chapter 1: Technical Armageddon: The burden of outdated IT systems

- Chapter 2: The digital facade: The failure of user experience (UX/UI)

- Chapter 3: Security vulnerabilities: A digital fortress or a house of cards?

- Conclusion: A strategic imperative for DARCA

- Sources

Technical Armageddon: the burden of outdated IT systems

While fintech startups build their platforms on flexible cloud architectures, the overwhelming majority of traditional banks continue to rely on IT infrastructure created in the 1970s and 1980s. Their reliability is an illusion that comes at an extremely high cost.

1.1. COBOL: a language from the past running the present

Info

The foundation of most banking mainframes is the programming language COBOL, created in 1959. The scale of its use is staggering: as of 2025, there are 344 billion lines of COBOL code worldwide, processing approximately $3 trillion in commercial transactions daily and underpinning 95% of all ATM transactions.

The problem is that specialists capable of working with these monolithic systems are retiring en masse, creating a talent crisis that The Financial Brand has described as an “astonishingly human threat”.

1.2. Frequent failures and multi-hour outages

Danger

The fragility of outdated systems is a harsh reality. An analysis by the UK Treasury Committee showed that over the past two years (2023-2024), the largest UK banks were collectively unavailable to customers for more than 803 hours due to IT failures. This is equivalent to 33 days of total downtime.

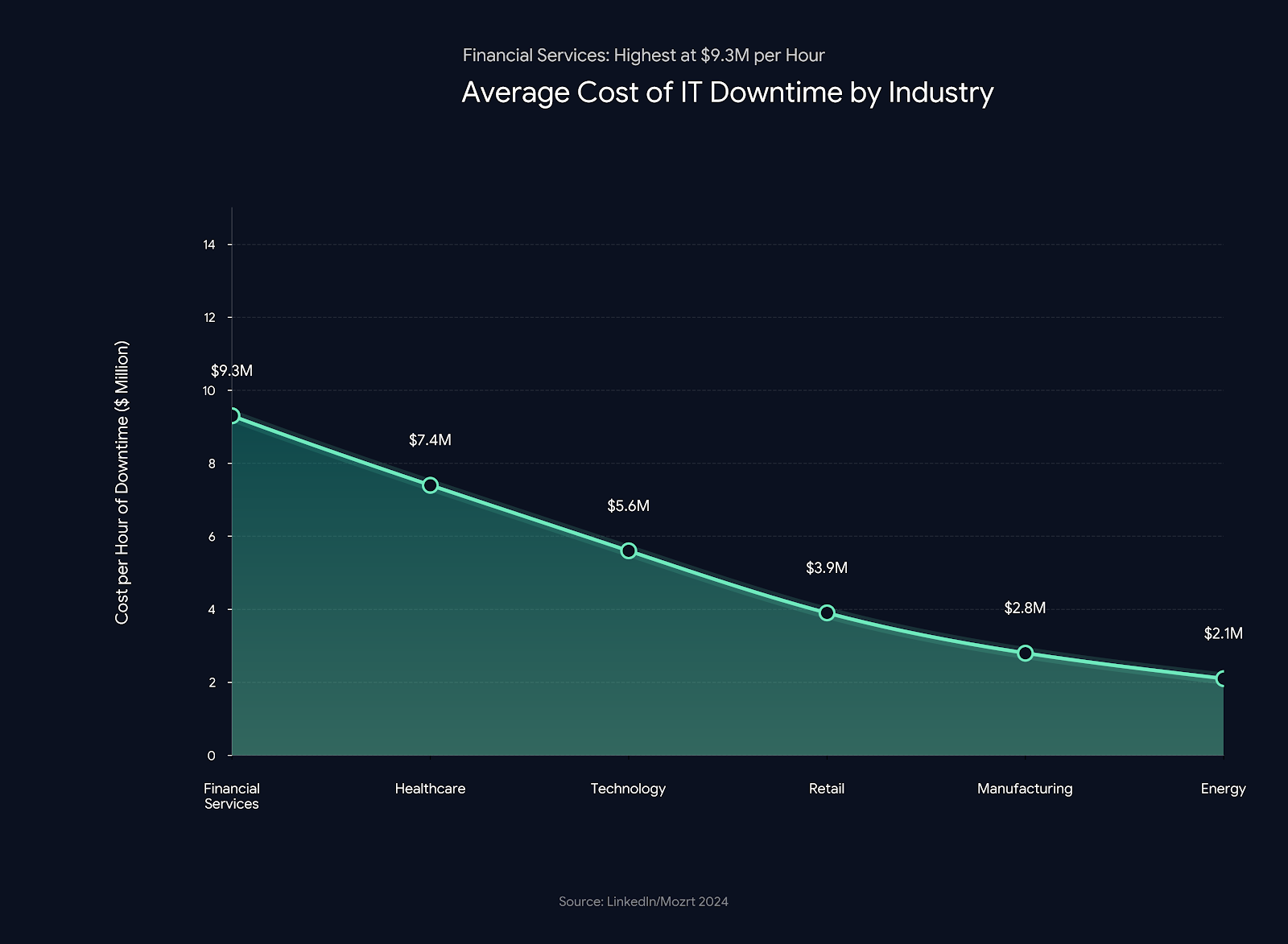

The leaders in downtime were NatWest (194 hours) and HSBC (176 hours). The cost of one hour of downtime in the financial sector is estimated at an average of $9.3 million.

Fig. 2. Cost of one hour of downtime by industry. The financial sector leads by a wide margin.

1.3. A brake on innovation: why banks cannot change

The most damaging consequence of outdated systems is the blockage of innovation. Banks spend enormous resources not on development, but on keeping their technological dinosaurs alive.

From 70% to 75% of the IT budget of an average bank goes to maintaining and servicing legacy systems. Less than one third of the budget remains for innovation.

This leads to the fact that 55% of bank executives name outdated systems as the main barrier to digital transformation, and 67% of US banks admit that they struggle to keep up with innovation in the payments space.

1.4. Technical debt: a ticking time bomb

Warning

All these problems form a massive technical debt. A 2025 study showed that 92% of bank executives are seriously concerned about the current level of technical debt and outdated systems.

Banks are trapped: a full replacement of the core system is a multi-billion-dollar project with enormous risks. However, inaction only exacerbates the problem, increasing operational risks and widening the gap with competitors.

Digital facade: failure of user experience (UX/UI)

If outdated core systems are a rotten foundation, then mobile applications are the facade. And it is here that banks’ failure becomes most visible to the user.

2.1. Outdated design and inconvenient interfaces

Despite years of investment in digitalization, 38% of users still experience frustration when using mobile banking in 2024. Improvement in this metric has virtually stalled since 2020.

A usability study of US banking websites clearly demonstrates a huge gap in UX quality. While some show strong results, others receive numerous complaints about complex navigation and difficulty finding information.

2.2. Comparison with leaders: why banks in Russia and Asia win

Info

The contrast between banking applications in the EU and the US and those in leading countries such as Russia is enormous. In numerous discussions on Quora and Reddit, users from Europe and the United States express admiration for the quality of Russian mobile banking:

“Why is mobile banking in Russia… so much better than in Europe? In Russia I can instantly transfer money to a friend through an app, while in France this may require a paper letter.” (Quora user)

The reason for this advantage is that the banking system in Russia was built almost from scratch, without the burden of outdated systems, which made it possible to implement modern IT solutions from the outset.

2.3. Business consequences of poor UX: loss of customers and revenue

Danger

Poor user experience is a direct threat to a bank’s business.

- 58% of customers are ready to switch banks due to a poor mobile application. This is the most common reason for switching banks.

- 67% of consumers will not choose a bank if it has a poor mobile application.

- Annual customer churn at traditional banks can reach 17.6%, which is 63% higher than that of digital competitors.

Improving the digital experience can increase a bank’s revenues by 20-30%. Failure in UX and UI is a strategic miscalculation that costs banks billions.

Security vulnerabilities: a digital fortress or a house of cards?

Banks position themselves as bastions of reliability, but their outdated IT systems are a source of colossal risks, turning digital fortresses into houses of cards.

3.1. DDoS attacks and ransomware: the financial sector under fire

Warning

The financial sector is the number one target for cybercriminals.

- In 2024, DDoS attacks on the financial sector increased by 49% quarter over quarter.

- 65% of financial organizations were hit by ransomware attacks in 2024, which is almost twice as much as in 2021.

3.2. Data breaches: millions of customers at risk

The complexity of legacy systems creates “blind spots” that attackers exploit.

The average cost of a data breach in the financial industry reached $6.08 million in 2024 - the highest figure across all industries.

The study showed that 97% of the 100 largest US banks were affected by data breaches through their third-party vendors in 2024. The largest breaches impacted tens of millions of people.

A strategic imperative for DARCA

The research conducted irrefutably proves that the banking sector in the EU and the United States is in a state of deep systemic crisis caused by technological backwardness.

- At the infrastructure level: Outdated core systems lead to outages, slow down transactions, and block innovation.

- At the user experience level: Inconvenient and non-functional applications cause mass frustration and customer churn.

- At the security level: Technological backwardness creates colossal vulnerabilities and undermines trust.

Info

This crisis creates enormous problems for consumers, but for DARCA it opens a unique window of opportunity. The unmet demand for modern, fast, and secure financial services is massive.

The DARCA platform, built on the principles of decentralization and advanced technologies, offers a direct solution to all identified problems.

The market is ready for a revolution. Traditional banks, shackled by the chains of their technological past, are unable to make the necessary changes. The strategic imperative for DARCA is to occupy this niche and become the new standard in the world of finance.

Sources

CodeAura.ai (2025). What 344 Billion Lines of COBOL Code Mean for the Future of Banking Tech. The Financial Brand (2025). Legacy Systems Under Siege, and the Threat is Human. Computer Weekly (2025). Big bank systems down for over 800 hours in last two years due to IT outages. LinkedIn / Mozrt (2024). The Hidden Costs of IT Downtime in 2024. Netguru (2025). Why Your Legacy Banking System is Holding You Back. Cari-tech.com (2024). The Hidden Cost of Banking Legacy Systems. Forbes / Finastra (2025). Reimagine banking: Innovation as the engine for differentiation. Banking Exchange (2024). Two-Thirds of US Banks Struggle to Keep Up with Payments Innovation. Tech Channels (2025). 92% are concerned about current levels of legacy systems and technical debt. OptimusAI (2025). Why Your Banking App Feels Like Homework (And Users Are Dropping Out). MeasuringU (2024). UX and NPS Benchmarks of Banking Websites (2024). Quora (2020). Why is mobile/internet banking so much better in Russia and China than in Europe? Reddit (2024). r/AskARussian - RU banking platform. Russia Beyond (2017). 8 most convenient online services from Russian banks. InvestForesight (2021). Fintech in Russia and the West: Similarities and differences. Euromoney (2025). The world’s best digital bank 2025: Revolut. The Asian Banker (2025). Nubank, ING (Global) and WeBank are the world’s top digital banks. EY (2024). Global Banking Consumer Study. Appcircle.io (2025). Most Popular Banking Apps in the US 2025 Data Analysis. McKinsey via Finextra (2025). Your App’s UX Is Not a Design Problem-It’s a Business Problem. Various Industry Reports (2024-2025). FS-ISAC & Akamai (2025). DDoS Attackers Increase Targeting of Global Financial Sector. Cloudflare (2024). DDoS Attack Threat Report Q3 2024. Fortinet (2025). Cybersecurity Statistics 2025: Rising Threats and Industry Trends. IBM (2024). Cost of a Data Breach Report 2024: Financial industry. SecurityScorecard (2024). Threat Intel Report: 97% of Leading U.S. Banks Impacted by Third-Party Data Breaches in 2024. American Banker (2024). The biggest data breaches of 2024 in financial services.