An invisible wall

Note

In today’s digital world, finance should be simple, fast, and unified. However, reality is far from this ideal. For both individuals and businesses, the financial landscape resembles a patchwork quilt of fragmented services, applications, and platforms. This phenomenon, known as service fragmentation, has become one of the most serious, yet often overlooked, problems of the modern financial system.

Users are forced to switch between dozens of applications: one for banking operations, another for buying cryptocurrency, a third for staking, a fourth for international transfers, a fifth for accounting and taxes. Each application has its own fees, limits, rules, and interface. This fragmentation creates not just inconvenience - it generates colossal financial losses, increases the risk of errors, complicates asset management, and slows down economic growth.

The purpose of this study is to thoroughly analyze the problem of fragmentation in financial and cryptocurrency services, prove its existence using concrete figures and facts, assess its destructive consequences, and demonstrate why solving this problem is critically important and opens up a massive strategic opportunity for DARCA.

We will prove that the market is desperately in need of a single, seamless ecosystem that unites traditional finance and cryptocurrencies. And DARCA is ready to become that ecosystem.

Table of contents

- Chapter 1: The great divide: the scale of fragmentation

- Chapter 2: The hidden tax: the economic cost of fragmentation

- Chapter 3: The user nightmare: risks, complexity, and lost time

- Chapter 4: Silent demand: the market craves consolidation

- Conclusion: Time to gather the stones

- Sources

The great divide: the scale of fragmentation

The problem of fragmentation is not a theoretical concept, but an everyday reality for hundreds of millions of people and companies. The scale of this problem is enormous and continues to grow.

1.1. The multiverse of applications

Info

The modern user is literally drowning in a sea of financial applications. Research shows that using multiple apps has become the norm rather than the exception.

According to a study by S&P Global Market Intelligence (August 2024), one third (33%) of US consumers use three or more financial applications to manage their money. Another 37% use two applications.

This trend is only intensifying. The growth of the FinTech industry has led to the emergence of thousands of narrowly specialized services, each solving only a single specific task.

1.2. Cryptocurrency chaos

In the world of cryptocurrencies, the situation is even more dramatic. Users are forced to rely on:

- Centralized exchanges (CEX) for buying and selling (Binance, Coinbase).

- Decentralized exchanges (DEX) for token swaps (Uniswap, PancakeSwap).

- Hardware wallets for secure storage (Ledger, Trezor).

- Software wallets for everyday transactions (MetaMask, Trust Wallet).

- Staking platforms for earning passive income (Lido, Rocket Pool).

- NFT marketplaces for trading digital assets (OpenSea, Magic Eden).

- Services for tax reporting (Koinly, CoinTracker).

Each of these services requires separate registration, key management, fee payments, and learning a new interface. This creates enormous barriers to the mass adoption of cryptocurrencies.

1.3. Business trapped

For businesses, fragmentation is not just an inconvenience, but a serious operational problem. Companies are forced to use separate solutions for payment acceptance, payroll, international settlements, liquidity management, and much more.

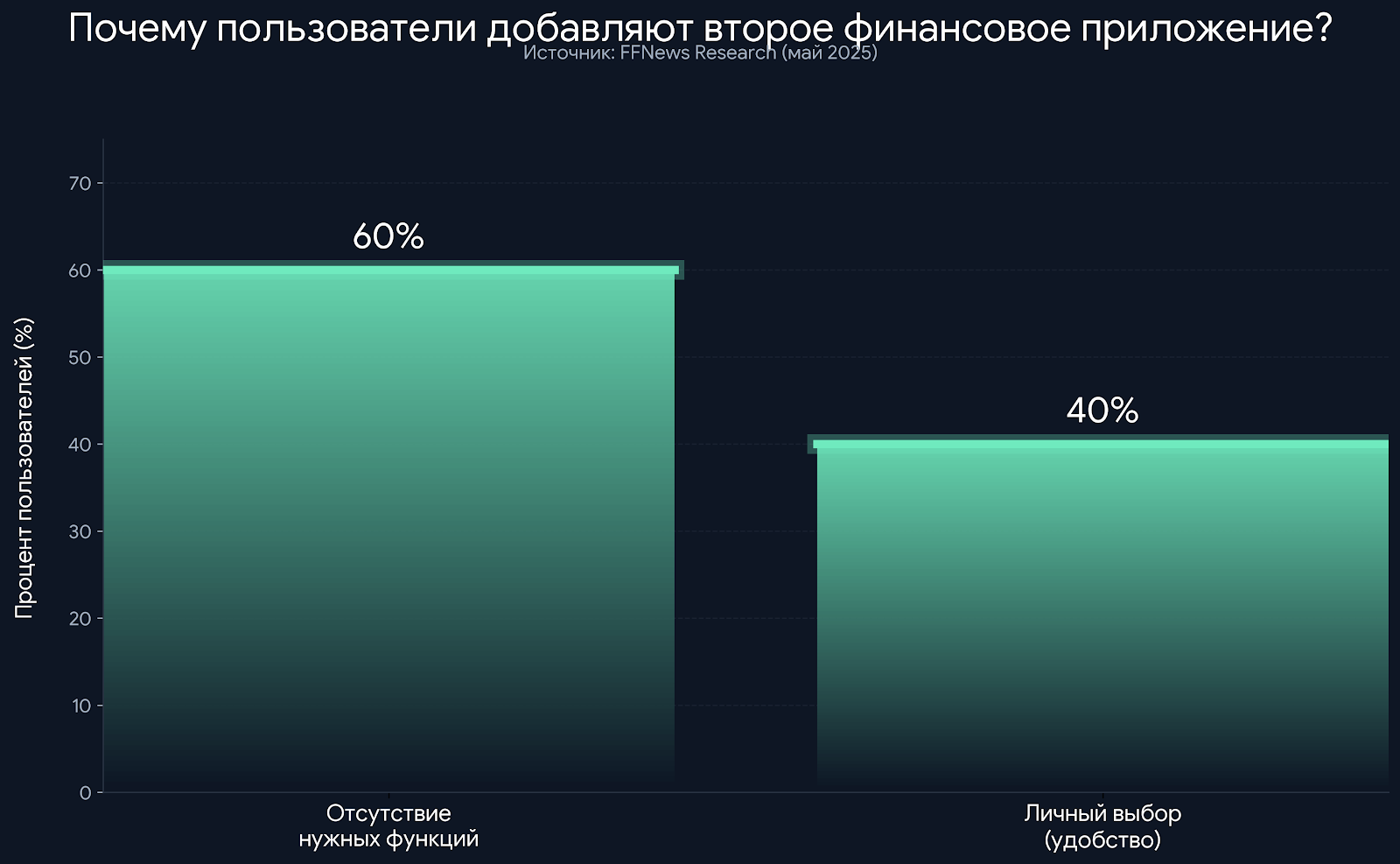

According to a study by FFNews (May 2025), 60% of users add a second financial application because their primary app lacks the required functionality.

This proves that existing solutions are incomplete and fail to meet customer needs, forcing users to seek alternatives and further exacerbating fragmentation.

Hidden tax: the economic cost of fragmentation

Fragmentation is not just an inconvenience. It is a massive, hidden tax on the global economy, measured in trillions of dollars.

2.1. Global economic losses

Danger

At the macro level, fragmentation of financial markets and regulatory regimes slows economic growth and creates systemic risks.

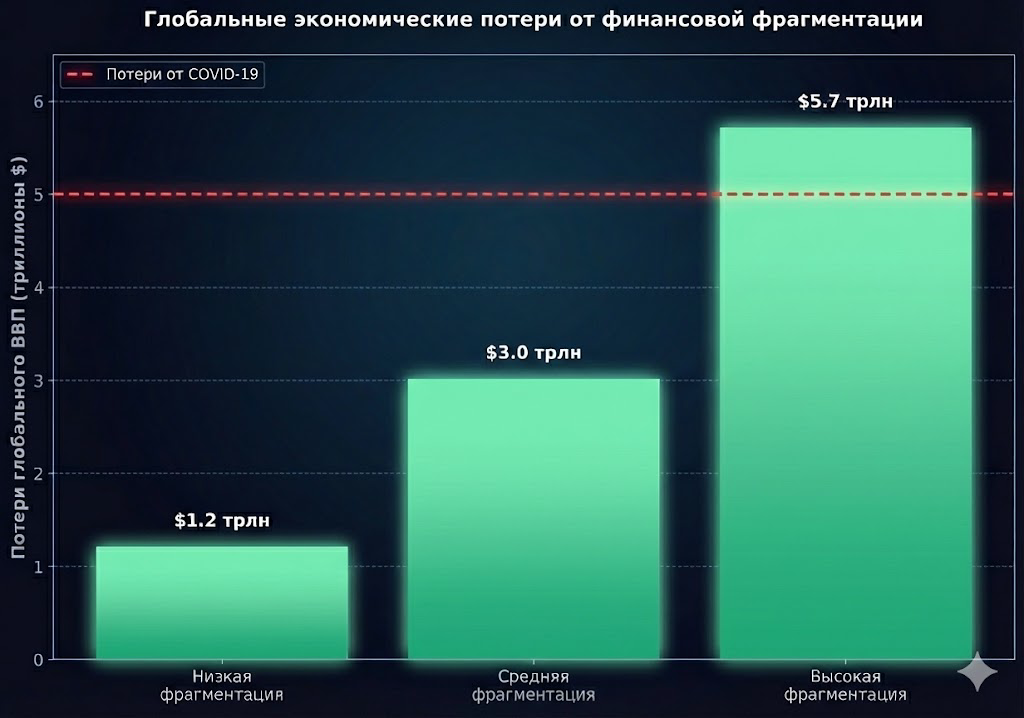

According to estimates by the World Economic Forum (January 2025), financial fragmentation could reduce global GDP by $5.7 trillion per year, exceeding the losses from the 2008 financial crisis or the COVID-19 pandemic.,

2.2. Losses from user errors

Warning

At the micro level, fragmentation leads to direct financial losses for users due to errors. In the world of cryptocurrencies, where transactions are irreversible, the cost of a mistake can be catastrophic.

According to Coinbase, due to user errors and smart contract bugs, more than 913,111 ETH worth $3.4 billion has been permanently lost. The increase in losses since 2023 amounted to 44%.,

One of the most common mistakes is sending cryptocurrency to the wrong network (for example, sending USDT on the BEP-20 network to an address on the ERC-20 network). This problem is a direct consequence of the fragmentation of the blockchain ecosystem.

2.3. Accounting and tax complexity

Fragmentation turns tax reporting into a real nightmare. Users must collect transaction data from dozens of platforms, which leads to errors, penalties, and enormous time costs. According to CNBC, the inability to properly report cryptocurrency transactions can result in audits and fines.

The user nightmare: risks, complexity, and lost time

Beyond the direct financial losses described in the previous chapter, fragmentation creates a whole range of non-financial, but no less serious, problems.

3.1. Increased security risks

Each new service is a new potential point of failure and a new target for hackers. Managing dozens of passwords and keys is a complex task that leads to vulnerabilities.

According to Chainalysis, in the first half of 2025 more than $2.17 billion was stolen from cryptocurrency services.

Fragmentation increases the attack surface and makes users more vulnerable to phishing, hacks, and fraud.

3.2. Cognitive overload and poor UX

Switching between dozens of applications with different designs and logic creates an enormous cognitive load. “Integration issues with other services” are among the main user complaints about financial applications. This problem is so severe that it can lead to catastrophic mistakes, as in the case of Citibank, whose employees accidentally sent $900 million to creditors due to a confusing interface.

3.3. Loss of time and efficiency

Time is one of the most valuable resources. Fragmentation relentlessly consumes it through registrations, transferring funds between platforms, learning interfaces, and collecting data for reporting. For businesses, these time costs translate into direct financial losses.

Silent demand: the market craves consolidation

Despite all the problems, users continue to rely on multiple services. This indicates that the market is desperately in need of a single, comprehensive solution.

4.1. Explosive growth of FinTech

Info

The rapid growth of the FinTech industry is the best evidence of user dissatisfaction with traditional banks.

According to DemandSage, in 2024-2025 64% of global consumers already use FinTech services. The number of digital banking users worldwide exceeded 2 billion people in 2025, showing a 35% increase since 2020.,

4.2. Readiness to switch to “super apps”

Users are tired of chaos. They are ready to abandon dozens of fragmented applications in favor of a single ecosystem. Convenience and the availability of all necessary features in one place are key factors when choosing a financial application. Demand for so-called “super apps” (Super-Apps) is growing rapidly.

4.3. A strategic opportunity for DARCA

The problem of fragmentation is not just a challenge, but a colossal market opportunity. A company that can offer a unified, secure, and convenient platform that brings together traditional and crypto finance has every chance to become a new industry standard.

DARCA was created precisely for this purpose. Our platform brings together in one place:

- Banking services (instant transfers, accounts).

- Cryptocurrency operations (exchange, storage, P2P exchange).

- Investment tools (staking, asset tokenization).

- Business solutions (acquiring, API integrations).

- Accounting and reporting tools.

By solving the problem of fragmentation, DARCA is not merely creating a convenient service. We eliminate multi-billion-dollar economic losses, reduce risks for users, and open access to modern financial tools for millions of people and companies.

Time to gather the stones

Note

The research clearly proves that fragmentation of financial services is one of the most acute and costly problems of the modern economy. It leads to:

- Trillion-dollar losses for the global economy.

- Billion-dollar losses for users due to errors and fraud.

- Increased security risks.

- Colossal time costs and cognitive overload.

- A slowdown of innovation and mass adoption of cryptocurrencies.

The market is ripe for a revolution. Users are tired of chaos and ready to move to a single, integrated platform. The silent demand for consolidation is enormous.

DARCA is in a unique position to lead this revolution. Our mission is to break down the invisible walls between services and create a single, seamless financial ecosystem. By eliminating fragmentation, we will not only capture the market, but also make a significant contribution to building a more efficient, secure, and accessible financial system for everyone.

The time to scatter stones has passed. The time to gather them has come. And DARCA is ready to begin.

Sources

S&P Global Market Intelligence. (2024, August). One-third of Americans use three or more financial apps. FFNews. (2025, May). Why do consumers add a second financial services app? World Economic Forum. (2025, January). Economic Costs of Fragmentation Could Eclipse Those of 2008 Financial Crisis or COVID-19 Pandemic. SWIFT. (2025, January). New report reveals high cost of financial fragmentation. CryptoSlate. (2025, July). Over 3.4B in ETH as Supply Losses Rise 44% Since 2023. CNBC. (2025, February). 3 common crypto mistakes to avoid when filing your 2024 taxes. Chainalysis. (2025, July). 2025 Crypto Crime Mid-Year Update. The UXDA. (2024). Banking Customers Aren’t Stupid; Your App Is Just Confusing. Medium. (2024). The Biggest Software Failures in the Financial and Banking Sector. DemandSage. (2025, August). FinTech Adoption Rate Statistics. Mobile Banking Statistics. (2025).