The main brake on the financial revolution

Note

The modern financial world stands on the brink of a revolution, yet its main brake is not technology, but people. More precisely, the inability of traditional banks to build effective and empathetic communication with clients. While fintech startups focus on delivering a flawless customer experience, large banking institutions continue to lose billions of dollars and the loyalty of millions of customers due to outdated approaches to service.

This study, conducted by the analytics team at DARCA, presents an in-depth analysis of the systemic crisis in customer service within the banking industry of the EU and the United States. We will prove that the problem does not merely exist - it has reached a critical scale. The report examines every aspect in detail: from hours-long waiting times on support lines and unqualified staff to failed automation and its catastrophic impact on customer loyalty.

Our goal is to demonstrate the massive market opportunity for companies capable of offering an alternative. For DARCA, this research serves as confirmation of the correctness of the chosen strategy, one that places the customer at its center.

Table of contents

- Chapter 1: The gap between expectations and reality: call centers and technical support

- Chapter 2: Automation failure: chatbots and IVR as a source of frustration

- Chapter 3: A crisis of trust: customer churn and declining loyalty

- Conclusion: A strategic opportunity for DARCA

- Sources

The gap between expectations and reality

The first line of defense of any bank is its customer support. However, for most clients it has become the first line of frustration.

1.1. Time is money that banks force customers to lose

In the era of instant messaging, waiting several hours for a response from a bank has become the norm. This is not just an inconvenience, but direct financial and reputational damage.

58% of customers complain that their bank responds too slowly when they need help.

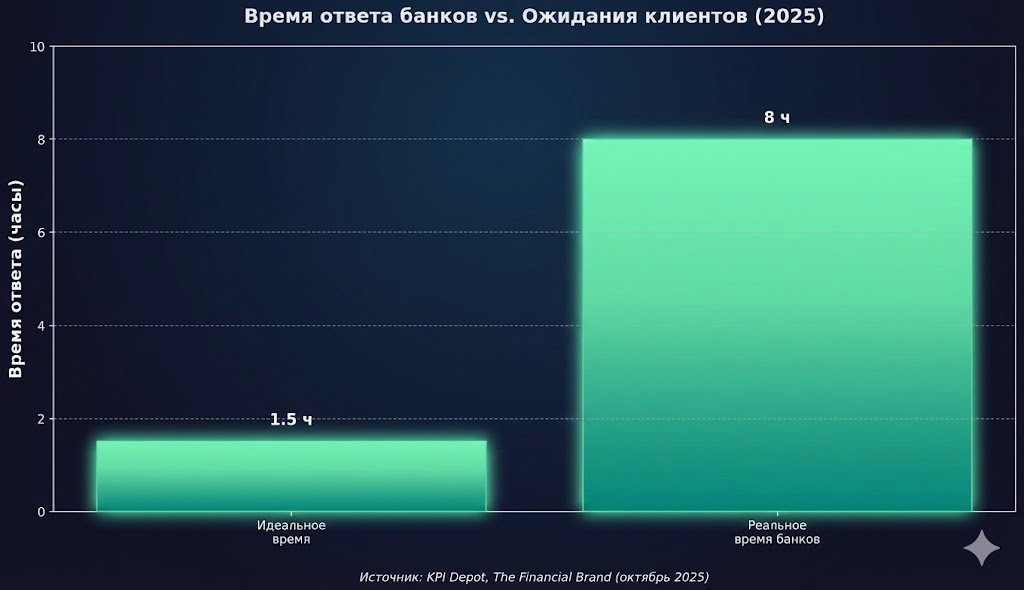

While the ideal response time should not exceed 1-2 hours, the reality of the banking sector is discouraging - average response times can reach 8 hours or more.

Chart 1: Comparison of actual bank response times with customer expectations. Sources: KPI Depot, The Financial Brand (October 2025).

1.2. Competence under question: why staff cannot help

Warning

Even if a client manages to get through, this does not guarantee that the issue will be resolved. The key support efficiency metric, FCR (First Contact Resolution), remains at a low level.

According to SQM Group, 30% of customers are forced to contact their bank again about the same issue.

This means that nearly every third call to a bank does not deliver a result due to insufficient staff training and a lack of decision-making authority. The problem is especially acute during business onboarding: 30% of companies require 4 or more contacts with a bank to resolve issues.

1.3. The outcome: loss of trust and customers

Low speed and lack of competence in customer support directly affect loyalty. 14% of customers are ready to leave for a competitor solely due to long response times.

Automation failure: chatbots and IVR as a source of frustration

In an attempt to cut costs, banks are massively deploying automated systems. However, instead of optimization, these technologies have become the primary source of negative experience.

2.1. “Fast but dumb”: why chatbots do not work

Danger

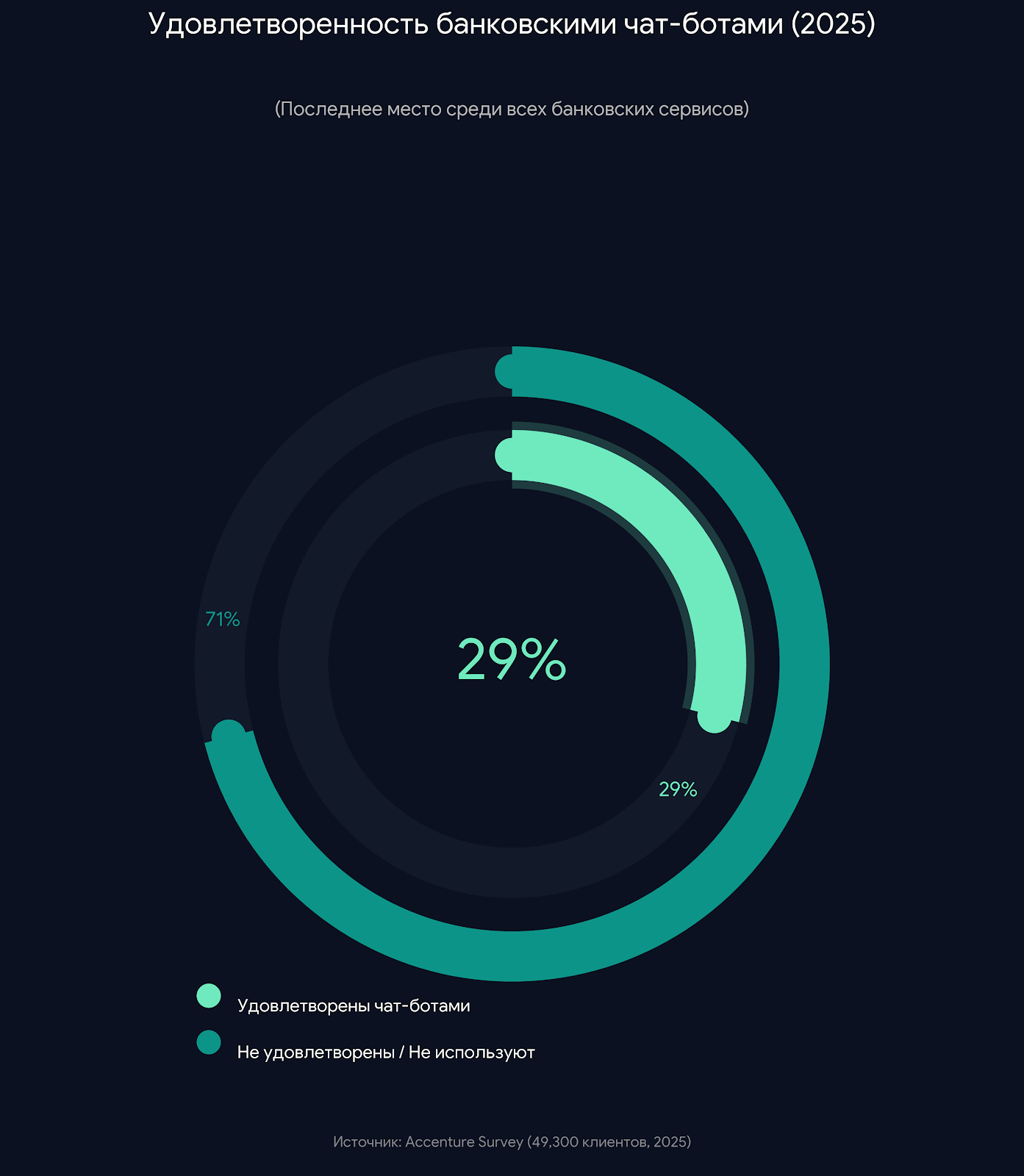

Despite the fact that 92% of banks in North America already use chatbots, satisfaction levels are at a record low.

According to an Accenture survey, only 29% of customers are satisfied with bank chatbots. This service ranked last in satisfaction among all banking services.

The main issues are the inability to understand complex requests and the lack of an easy way to reach a live agent. The consequences are catastrophic: 30% of customers are ready to leave after a single negative experience with a chatbot.

Chart 3: Customer satisfaction level with banking chatbots. Source: Accenture Survey (2025).

2.2. IVR: labyrinths with no exit

Voice menus (IVR) have turned into confusing labyrinths that cause nothing but frustration for customers.

61% of customers associate negative IVR experiences with overall poor service quality, and 51% admit that they have completely abandoned a business due to the inability to get through automated menus.

2.3. Failed onboarding: losing the customer at the very start

Warning

Automation issues are especially acute during the onboarding process.

According to various estimates, 50% to 63% of digital applications for opening a bank account are never completed.

Banks lose customers before they even become customers due to overly complex and lengthy processes. According to Forrester, 64% of banks directly lose revenue because of these issues.

A crisis of trust: customer churn and declining loyalty

Low service quality, compounded by high fees and outdated technologies, has led to a systemic crisis of trust. Customers are not merely dissatisfied - they are actively seeking alternatives.

3.1. Voting with their feet: a mass customer exodus

Info

Poor service quality has become the second most important reason for switching banks, after high fees.

39% of customers are ready to leave their bank for this very reason.

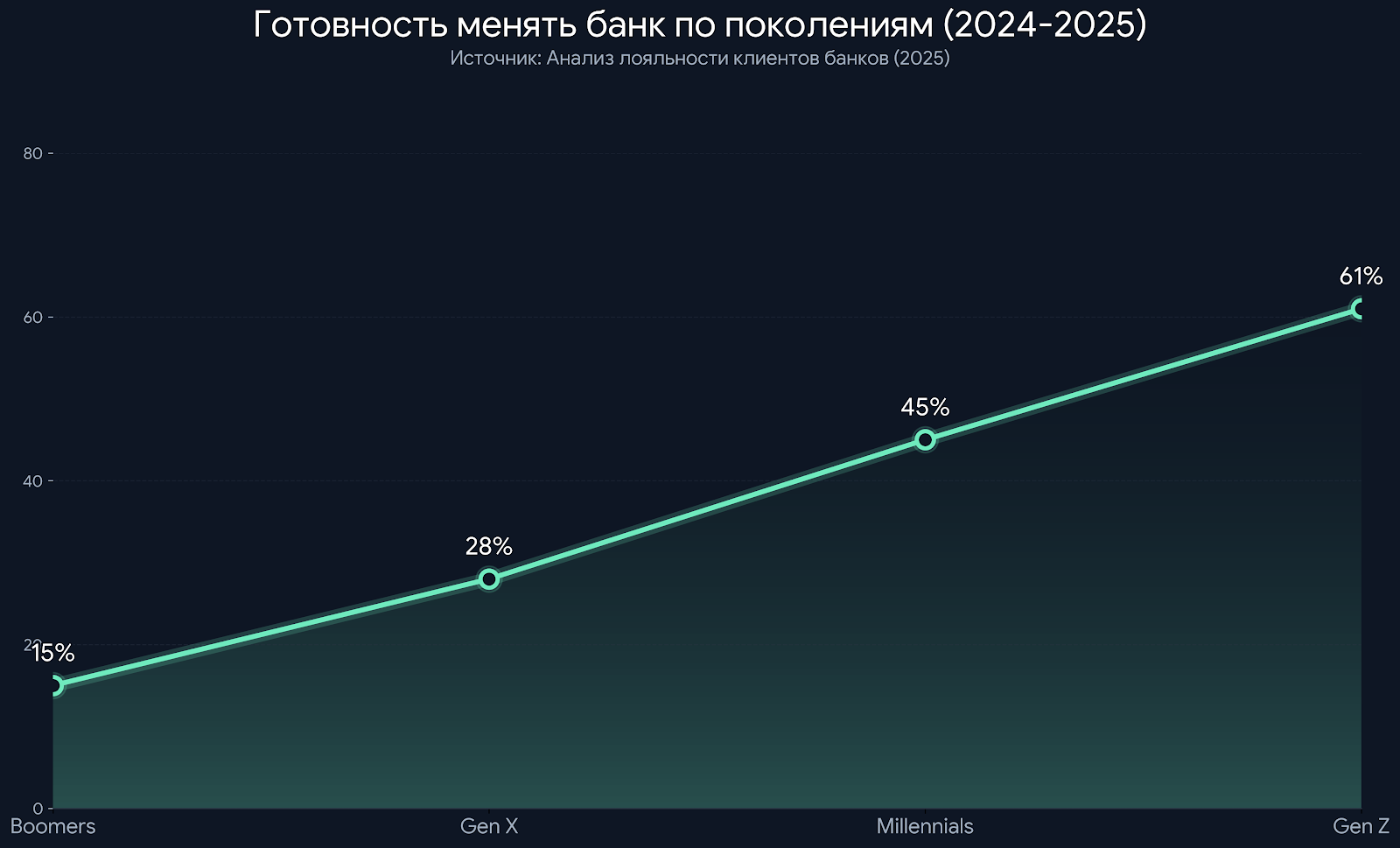

This trend is especially pronounced among younger generations. 61% of Generation Z have already switched banks over the past two years. They grew up in a digital environment and are unwilling to tolerate archaic service.

Chart 8: Percentage of customers who switched banks over the past 2 years. Source: Bank customer loyalty analysis (2025).

3.2. Neobanks as an alternative

This customer outflow flows directly into neobanks and fintech services. A comparison of retention metrics clearly demonstrates the advantage of digital players.

The churn rate of traditional banks (17.6%) is 63% higher than that of digital banks (10.8%).

This proves that customers deliberately choose providers with a better customer experience, rather than simply leaving “into nowhere”.

A strategic opportunity for DARCA

The research conducted unequivocally proves that the banking sector in the EU and the United States is in a state of deep customer service crisis.

Key conclusions:

- The problem is large-scale: Tens of millions of customers are dissatisfied, and financial losses amount to billions.

- The problem is universal: It affects all communication channels (from call centers to chatbots) and all stages of the customer journey.

- Customers are ready for change: The younger generation is actively seeking and switching to providers that offer modern service.

For DARCA, this confirms a massive market opportunity. Our platform, with a focus on instant transactions and a flawless digital experience, is a direct response to all of these challenges. We can offer what traditional banks are unable to deliver:

- Efficient and competent 24/7 support.

- Transparency and speed in resolving any issues.

- An omnichannel experience without loss of context.

The market is ready for a revolution in customer service. And DARCA is ready to lead it.

Sources

The Financial Brand. (2025, October 7). Response Time is a Persistent Customer Pain Point. SQM Group. (2025, November 14). First Call Resolution (FCR): A Comprehensive Guide. Ovation CXM. (2022, December 8). 30% of Businesses Report 4+ Contacts Needed to Solve Banking Onboarding Issues. Frank RG. (2024). Исследование качества клиентского обслуживания в банковском секторе. Accenture. (2025). Global Banking Consumer Study 2025. Forbes. (2023, February 1). One Negative Chatbot Experience Drives Away 30% Of Customers. Assembled. (2025, April 8). Why customers hate IVR (and how you can fix it). VCC Live. Call abandonment rate - Basics, common mistakes. The Financial Brand. (2025, August 14). More Than Half of Customers Abandon Account Opening. Innovatrics. (2020). 63% of customers abandon digital bank onboarding. Forrester Research, cited in Lightico blog. Lost Customers, Lost Dollars: How Bad Onboarding is Bleeding Your Bank Dry. Анализ лояльности клиентов банков. (2025). (Загруженный документ). J.D. Power. (2025). 2025 U.S. Retail Banking Satisfaction Study. FBF-IFOP. (2024). French Banking Federation Survey. Mintel. (2025). UK Retail Banking Report. FICO/McKinsey. (2024). German Banking Customer Survey. KPI Depot. Customer Support Response Time KPI. Zendesk. (2025, August 12). What is first contact resolution (FCR)?. Balto. (2025, June 27). Measure & Improve First Contact Resolution in a Call Center. Vonage. (2025, April 15). The Horrors of IVR: Five Key Issues. Geckoboard. Call Abandonment Rate KPI Example.